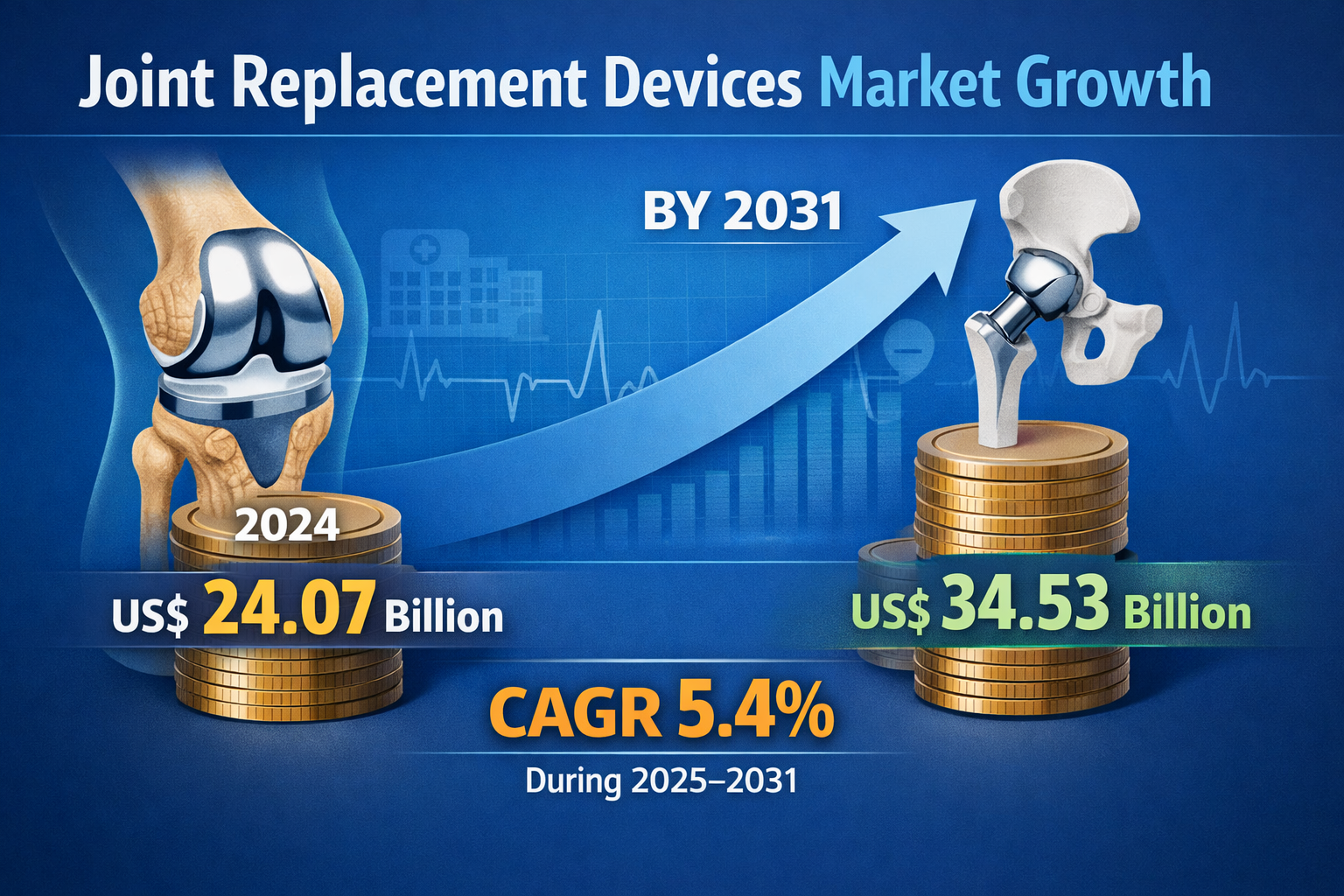

The global orthopedic sector is entering a transformative era, shifting from purely mechanical solutions to sophisticated, data-integrated ecosystems. The Joint Replacement Devices Market is a cornerstone of this evolution, projected to reach a valuation of US$ 34.53 billion by 2031. This growth, rising from US$ 24.07 billion in 2024 at a steady CAGR of 5.4%, is underpinned by a confluence of demographic necessity and rapid technological disruption.

As healthcare systems globally move toward value-based models, the market overview reveals an industry focused on enhancing surgical precision, reducing hospital stays, and personalizing patient outcomes.

Download Sample PDF Copy of Joint Replacement Devices Market Size and Growth Drivers 2031 at: https://www.theinsightpartners.com/sample/TIPRE00025004

Core Market Dynamics: Drivers and Constraints

The momentum of the joint replacement industry is driven by structural shifts in global health profiles and the technological tools designed to address them.

-

The Aging Global Demographic: The primary engine of market growth is the "Silver Tsunami." By 2030, the global population aged 60 and over is expected to reach 1.4 billion. This demographic shift significantly increases the prevalence of age-related bone diseases, such as osteoarthritis and osteoporosis, which necessitate joint reconstruction to maintain mobility and quality of life.

-

Obesity and Early-Onset Joint Decay: Rising global obesity rates (currently affecting 13% of the population) have created a secondary surge in demand. Increased body mass accelerates the wear and tear of weight-bearing joints, leading to a rising number of younger patients in their 40s and 50s requiring primary knee and hip replacements.

-

Technological Precision: Innovation in robotic-assisted surgery (RAS) and 3D printing has redefined the limits of joint replacement. Robotics, like Stryker’s Mako and Zimmer Biomet’s ROSA, have reduced alignment errors to under 0.5 degrees, while 3D-printed porous titanium implants offer superior bone ingrowth compared to traditional materials.

-

Economic Barriers: Despite high demand, the market faces restraints in the form of high procedure costs and inconsistent reimbursement policies in emerging economies. In regions like India or Brazil, the lack of widespread private insurance can limit access to premium technologies like robotic surgery, which often carries a 10% premium over traditional methods.

Strategic Market Segmentation

The joint replacement market is a multifaceted industry segmented by the type of joint, the fixation method, and the technology employed.

-

By Product Type:Knee replacements remain the largest segment, accounting for over 40% of the market share. This dominance is due to the high incidence of knee osteoarthritis and the success of total knee arthroplasty (TKA). However, shoulder replacements are emerging as the fastest-growing sub-segment, driven by advancements in reverse shoulder designs and improved surgical indications.

-

By Fixation Type: While cemented fixation has traditionally been the gold standard for older patients due to its immediate stability, cementless (biological) fixation is gaining ground. This method is preferred for younger, more active patients as it promotes natural bone ingrowth, potentially extending the implant’s lifespan.

-

By Technology: Conventional surgeries still hold the majority share, but robotic-assisted and AI-guided procedures are the high-growth outliers. These technologies are increasingly favored in Ambulatory Surgical Centers (ASCs), where precision and fast recovery are essential for same-day discharge models.

Geographical Landscape: Consolidation vs. Expansion

The geographical overview highlights a clear divide between revenue-generating mature markets and volume-driving emerging regions.

-

North America: Commands the largest revenue share, approximately 45.6%. Its leadership is cemented by an advanced healthcare infrastructure, high healthcare expenditure, and the rapid transition of surgeries to outpatient settings. The U.S. remains the primary launchpad for "smart" implants and digital surgery platforms.

-

Asia-Pacific: Positioned as the fastest-growing region, APAC is fueled by massive patient populations in China and India. Government initiatives to control implant prices and the expansion of private hospital chains are making joint replacements more accessible to millions, while medical tourism in countries like Thailand continues to bolster regional growth.

Future Outlook: The Era of Smart Orthopedics

Looking toward 2031, the market is expected to pivot from "hardware sales" to "comprehensive care delivery." The integration of Smart Implants devices embedded with sensors to track gait, temperature, and range of motion will turn every artificial joint into a diagnostic tool. This data-driven approach will allow surgeons to monitor patients remotely, detecting early signs of infection or wear before they require expensive revision surgeries.

As the industry consolidates, the winners will be those who successfully bridge the gap between high-tech precision and cost-effective accessibility, ensuring that the next generation of orthopedic care is as durable as it is innovative.

Trending Reports :

About Us:

The Insight Partners provides comprehensive syndicated and tailored market research services in the healthcare, technology, and industrial domains. Renowned for delivering strategic intelligence and practical insights, the firm empowers businesses to remain competitive in ever-evolving global markets.

Contact Information -

Email: sales@theinsightpartners.com

Phone: +1-646-491-9876

Also Available in : Korean| German| Japanese| French| Chinese| Italian| Spanish